What’s next

Public Mint continues to work on its features, like EARN and the web wallet. It’s also looking into adding debit card compatibility and possibly loans. And since Hyperledger Besu is enterprise-ready, it’s also looking to open the platform to corporations

Already a few companies have integrated with it for instant transactions and microtransactions that allow a fiat-native settlement with their customers. And community developers are working on other promising use cases like decentralized exchanges and non-fungible token (NFT) marketplaces.

Beyond those uses, Public Mint sees scaling to even larger applications in supply chain finance. This corporate use would be a challenge to develop without Hyperledger Besu. “We’re very happy to have chosen Pantheon, which is now Hyperledger Besu,” says Rodriques. “It will naturally catalyze quick integration with corporations.”

And creative corporate use cases are exactly what Public Mint is after.

“We’re firm believers that a lot of innovation is happening in the blockchain space, but the ‘crypto bubble’ still constrains it,” says Rodrigues. “It’s not reaching mainstream users, which is why a lot of interesting use cases and solutions haven’t yet reached mass adoption. But there is a world of use cases out there. Some of them we can’t even imagine yet.”

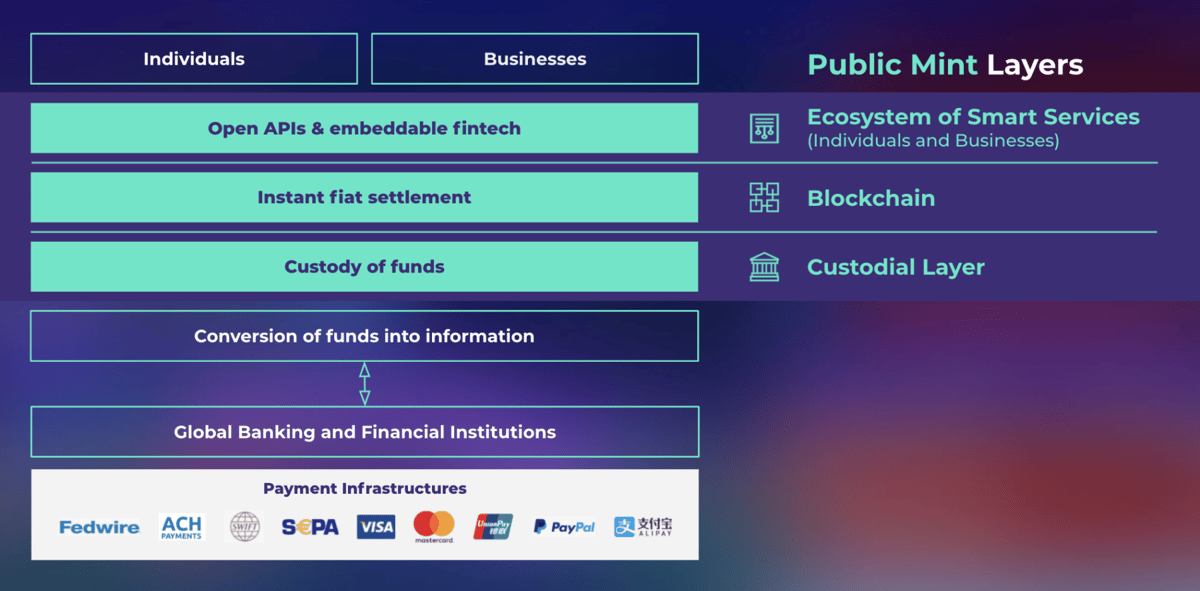

System graphic

About Public Mint

Public Mint is an open blockchain blended with an API platform that allows regular money to get all the superpowers of a cryptocurrency, minus the volatility, complexity and regulatory uncertainties depending on the geographies. People and businesses from all over the world are free to build all kinds of money-based applications and services on top of Public Mint, fueled by money as we know it – without the limitations of traditional banking rails. The company was founded in 2018 and has offices in the US, UK and Europe. To learn more, visit https://publicmint.com/

About Hyperledger

Hyperledger Foundation was founded in 2015 to bring transparency and efficiency to the enterprise market by fostering a thriving ecosystem around open source blockchain software technologies. As a project of the Linux Foundation, Hyperledger Foundation coordinates a community of member and non-member organizations, individual contributors and software developers building enterprise-grade platforms, libraries, tools and solutions for multi-party systems using blockchain, distributed ledger, and related technologies. To learn more, visit https://www.hyperledger.org/